In residential real estate, an appraisal is an estimation of a specific property’s fair market value. As part of a real estate transaction, it assures the buyer, the seller and the lender that the agreed upon purchase price is fair.

Since Red Oak is engaged in selling and buying real estate, the focus here is on how appraisals function in transactions. They’re also used in a number of other circumstances ranging from a mortgage refinance to divorce and estate settlement.

It’s important to note that value is not the same as cost or price:

- Cost is the dollar amount needed to build or buy the exact same property in the current market

- Price is what a buyer actually pays for the property

- Value is what the appraiser believes a buyer would be willing to pay for the property based on their evaluation

According to the California Department of Real Estate, the appraisal provides “the most probable price which a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus.”

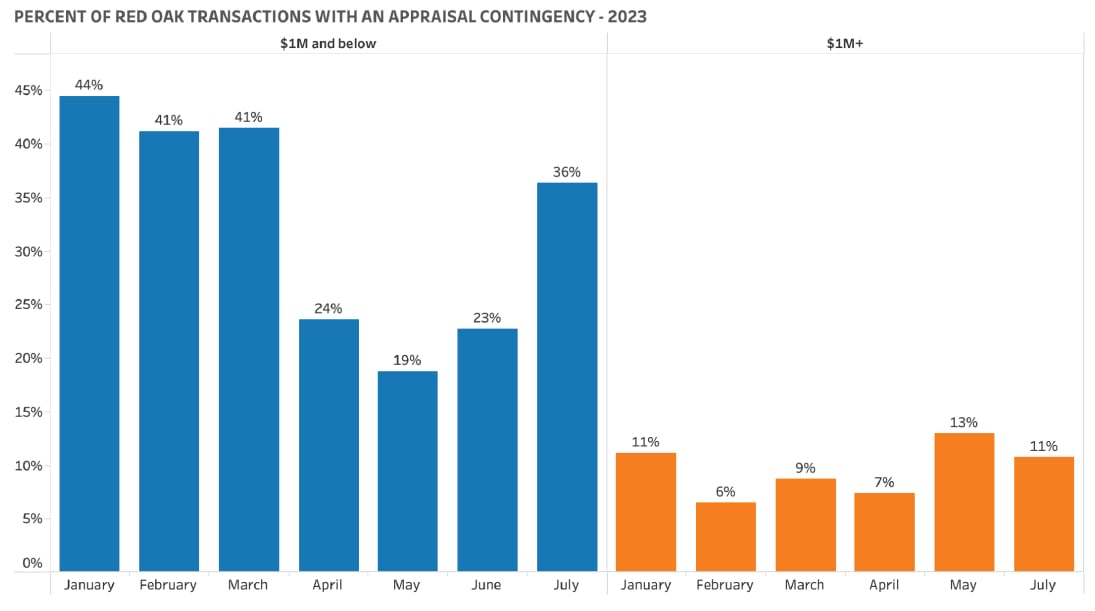

If a buyer needs a mortgage to buy a home (or even if they're paying cash), their agent will probably suggest including an appraisal contingency in the sales contract. This allows the buyer to walk away if the appraisal comes in below the agreed upon purchase price. Based on Red Oak’s internal data, appraisal contingencies are used at all price points, but are more common in transactions with a sale price under $1M.

The Process

In compliance with the Dodd-Frank Act, your chosen lender will be the one to initiate the appraisal process. The appraiser must be appropriately trained and licensed by the California Bureau of Real Estate Appraisers. Just like most services, the length of time it takes to complete the report will depend on the appraiser’s workload and the complexity of the assignment. In the East Bay, all those involved understand that this is time sensitive.

The appraiser will visit the property, inspect the interior and exterior, take photos, measure the square footage, evaluating the home's features, fixtures and overall condition. They will then research recent comparable sales (comps). A minimum of 3 comps should be included. They should be homes that sold no more than 6 months prior, be located in the same neighborhood and be similar in size and condition.

The Appraisal Report Includes:

- A street map showing the location of the subject property and comps used

- A parcel map showing property lines and measurements

- A floor plan with measurements

- An explanation of how the square footage was calculated

- Photographs of the home’s exterior, interior rooms, and street

- Front exterior photographs of each comp

- Any other pertinent information such as market sales data, public land records, and public tax records that have been used

The appraiser provides an analysis and conclusions about the property's value based on this data, but an accurate appraisal is both science and art. The appraiser then adjusts the subject property’s valuation relative to the differences in the comps. Personal judgment and even intuition can’t be completely eliminated in the appraisal process, and this is one more reason to work with local experts.

When the appraisal comes in at or above the purchase price, an important milestone has been reached on the way to home ownership!

What if the Appraisal is Lower than Expected?

A low appraisal is not an uncommon glitch, especially in a rapidly changing market. Depending on the specifics, the buyer’s agent may be able to negotiate with the seller’s agent to lower the purchase price. The buyer may come up with the difference between the contract price and the appraised value or they may decide to exercise that appraisal contingency and cancel the sale.

The agent can also help the buyer challenge the appraisal by presenting additional comps or other data to support a higher valuation. In some instances, it may be appropriate to work with the lender and find another appraiser with more local market awareness for a do-over.

It is sadly necessary to point out that appraisals can be affected by bias. Anyone who thinks they have encountered such a dubious situation, should speak up immediately!

The appraisal process is one of many real estate complexities. At Red Oak we endeavor to educate, simplify and guide our clients through the maze. If we can clarify or help interpret information, reach out, we’d love to help.