The market suffered significant declines when the COVID-19 pandemic hit us in mid-March, but the market has improved and demand remains strong. Here are a few key takeaways from our 87-page analysis.

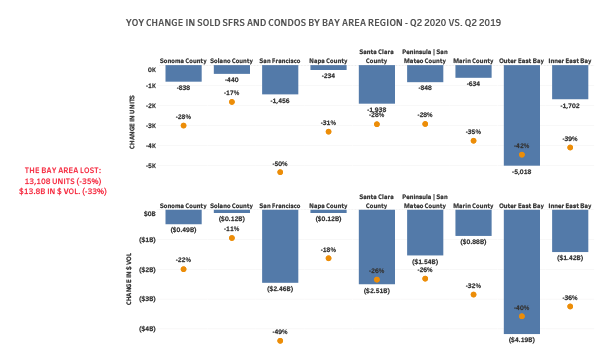

The Bay Area lost $13.8 billion worth of transactions in Q2 2020 compared to 1 year ago. San Francisco fared the worst, with units and dollar volume falling by 50%.

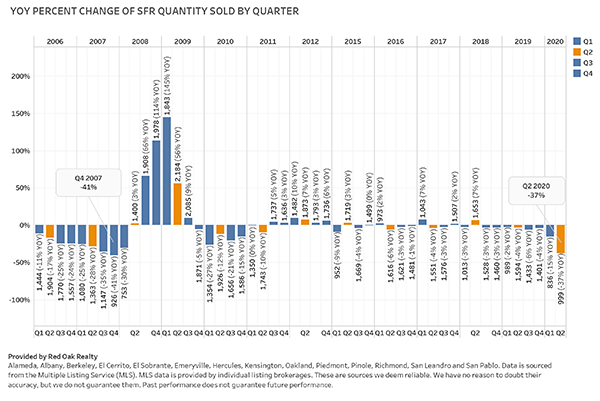

What’s more, the number of single family homes had its worst quarter since the Great Recession. Units fell 37% in Q2 2020 vs. 1 year ago; they fell 47% in Q4 2007. Much of this decline was caused by a lack of available homes for sale.

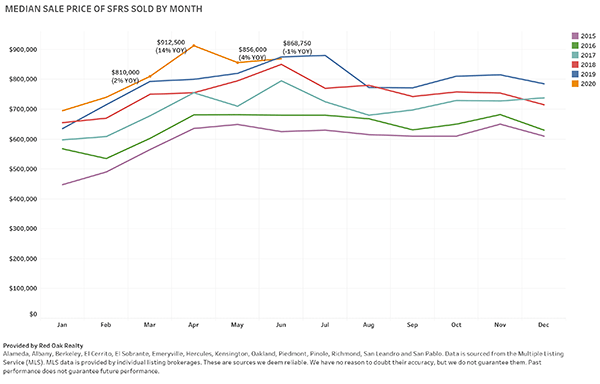

Prices have not suffered the same decline. They remain at or above last year‘s levels: as of June the median was $868,750, down 1% since last year and up 5% year to date.

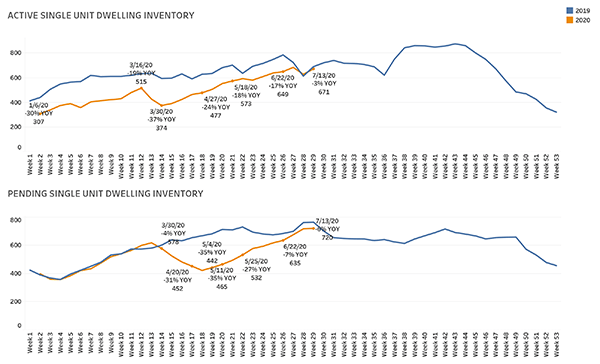

Since the end of Q2, supply has increased dramatically with active inventory just 3% below 2019 and properties pending under contract at 6% below 2019.

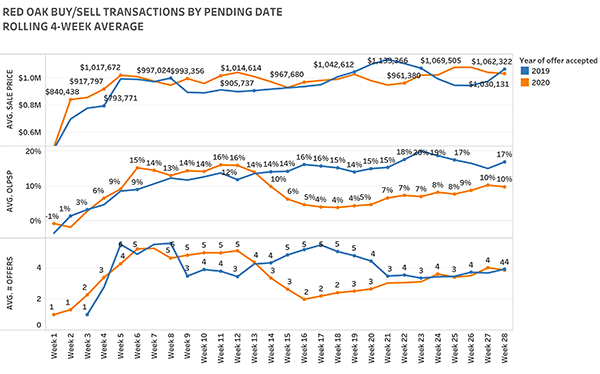

Demand is also on the rise. Based upon Red Oak transactions, properties are attracting an average of 4 offers and selling an average of 10% above list price.

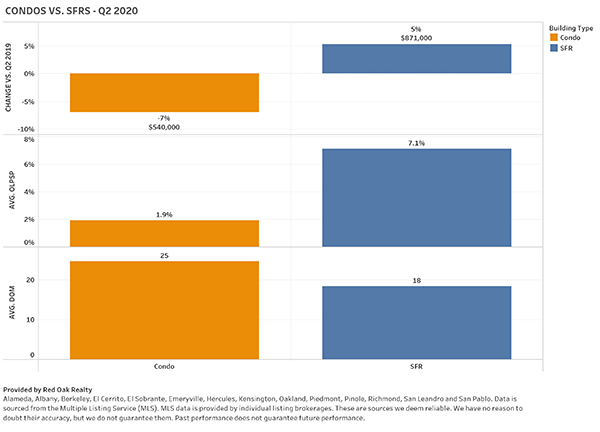

But not all properties performed equally. Condo values fell 7% and are taking longer to sell than single family homes, likely due to the separation of space that many people are looking for when buying a home during COVID.

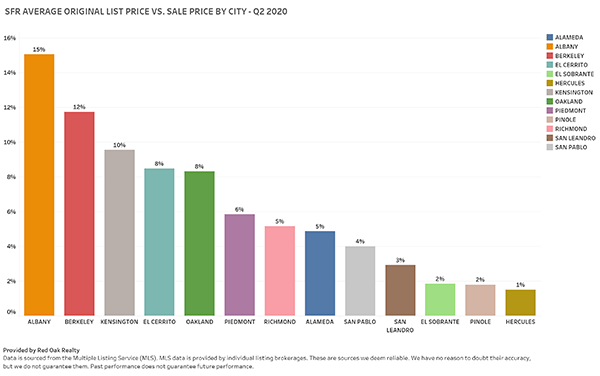

Albany outperformed other cities in the inner East Bay: it was the only city that had an increase in sales, prices increased more than any other city (17% YOY), homes sold faster (14 days on market) and further over asking (15%) – the highest in the entire Bay Area.

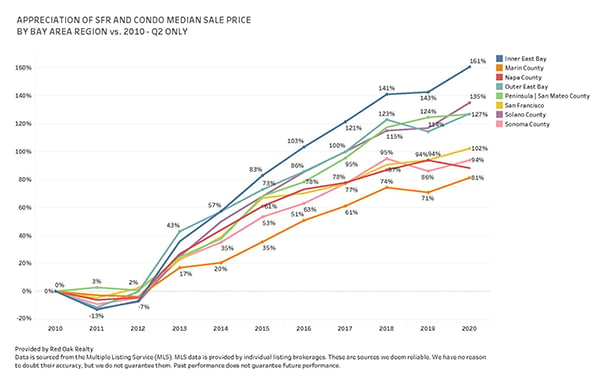

The East Bay continues to outperform other Bay Area regions as values have appreciated 161% since 2010.

Click here to download the entire report, and if you’d like a custom analysis of your neighborhood, please let us know.